Abstract

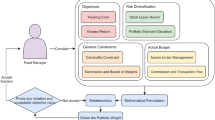

In recent years the popularity of indexing has greatly increased in financial markets and many different families of products have been introduced. Often these products also have a minimum guarantee in the form of a minimum rate of return at specified dates or a minimum level of wealth at the end of the horizon. Periods of declining stock market returns together with low interest rate levels on Treasury bonds make it more difficult to meet these liabilities. We formulate a dynamic asset allocation problem which takes into account the conflicting objectives of a minimum guaranteed return and of an upside capture of the risky asset returns. To combine these goals we formulate a double tracking error problem using asymmetric tracking error measures in the multistage stochastic programming framework.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Preview

Unable to display preview. Download preview PDF.

Similar content being viewed by others

References

Alexander, G.J., Baptista, A.M.: Portfolio selection with a drawdown constraint. J. Banking Finan. 30, 3171–3189 (2006)

Barro, D., Canestrelli, E.: Tracking error: a multistage portfolio model. Ann. Oper. Res. 165(1), 44–66(2009)

Basak, S.: A general equilibrium of portfolio insurance. Rev. Finan. Stud. 8, 1059–1090 (1995)

Basak, S., Shapiro, A., Tepla, L.: Risk management with benchmarking. Working paper series asset management SC-AM-03-16, Salomon Center for the Study of Financial Institutions, NYU (2003)

Boyle, P., Tian, W.: Optimal portfolio with constraints. Math. Finan. 17, 319–343 (2007)

Brennan, M., Solanki, R.: Optimal portfolio insurance. J. Finan. Quant. Anal. 16, 279–300 (1981)

Browne, S.: Beating a moving target: optimal portfolio strategies for outperforming a stochastic benchmark. Finan. Stochastics 3, 255–271 (1999)

Consiglio, A., Cocco, F., Zenios, S.A.: The Prometeia model for managing insurance policies with guarantees. In: Zenios, S.A. and Ziemba, W.T. (Eds.) Handbook of Asset and Liability Management, vol. 2, pp. 663–705. North-Holland (2007)

Consiglio, A., Saunders, D., Zenios, S.A.: Asset and liability management for insurance products with minimum guarantees: The UK case. J. Banking Finan. 30, 645–667 (2006)

Deelstra, G., Grasselli, M., Koehl, P.-F.: Optimal investment strategies in the presence of a minimum guarantee. Ins. Math. Econ. 33, 189–207 (2003)

Deelstra, G., Grasselli, M., Koehl, P.-F.: Optimal design of the guarantee for defined contribution funds. J. Econ. Dyn. Control 28, 2239–2260 (2004)

Dembo, R., Rosen, D.: The practice of portfolio replication, a practical overview of forward and inverse probems. Ann. Oper. Res. 85, 267–284 (1999)

Dempster, M.H.A., Thompson, G.W.P.: Dynamic portfolio replication usign stochastic programming. In: Dempster, M.H.A. (ed.) Risk Management: Value at Risk and Beyond, pp. 100–128. Cambridge Univeristy Press (2001)

Dempster, M.A.H., Germano, M., Medova, E.A., Rietbergen, M.I., Sandrini, F., and Scrowston, M.: Designing minimum guaranteed return funds. Research Papers in Management Studies, University of Cambridge, WP 17/2004 (2004)

El Karoui, N., Jeanblanc, M., Lacoste, V.: Optimal portfolio management with American capital guarantee. J. Econ. Dyn. Control 29, 449–468 (2005)

Franks, E.C.: Targeting excess-of-benchmark returns. J. Portfolio Man. 18, 6–12 (1992)

Gaivoronski, A., Krylov, S., van der Vijst, N.: Optimal portfolio selection and dynamic benchmark tracking. Eur. J. Oper. Res. 163, 115–131 (2005)

Grossman, S.J., Zhou, Z.: Equilibrium analysis of portfolio insurance. J. Finan. 51, 1379–1403 (1996)

Halpern, P., Kirzner, E.: Quality standards for index products. Working paper. Rotman School of Management, University of Toronto (2001)

Hochreiter, R., Pflug, G., Paulsen, V.: Design and management of Unit-linked Life insurance Contracts with guarantees. In: Zenios, S.A. and Ziemba W.T. (eds.) Handbook of asset and liability management vol. 2, pp. 627–662. North-Holland (2007)

Jensen, B.A., Sorensen, C.: Paying for minimal interest rate guarantees: Who should compensate whom? Eur. Finan. Man. 7, 183–211 (2001)

Konno, H., Yamazaki, H.: Mean absolute deviation portfolio optimization model and its applications to Tokyo stock market. Man. Sci. 37, 519–531 (1991)

Lintner, J.: The valuation of risky assets and the selection of risky investments in stock portfolios and capital budget. Rev. Econ. Stat. 47, 13–37 (1965)

Michalowski, W., Ogryczak, W.: Extending the MAD portfolio optimization model to incorporate downside risk aversion. Naval Res. Logis. 48, 185–200 (2001)

Mossin, J.: Equilibrium in a Capital Asset Market. Econ. 34, 768–783 (1966)

Muermann, A., Mitchell, O.S., Volkman, J.M.: Regret, portfolio choice, and guarantees in defined contribution schemes. Insurance: Math. Econ. 39, 219–229 (2006)

Rudolf, M., Wolter, H.-J., Zimmermann, H.: A linear model for tracking error minimization. J. Banking Finan. 23, 85–103 (1999)

Sharpe, W.F.: Capital asset prices: a theory of market equilibrium under conditions of risk. J. Finan. 19(3), 425–442 (1964)

Sorensen, C.: Dynamic asset allocation and fixed income management. J. Finan. Quant. Anal. 34, 513–531(1999)

Zenios, S.A., Ziemba, W.T. (eds.): Handbook of Asset and Liability Management, vol. 2. North-Holland (2007)

Ziemba, W.T.: The Russel-Yasuda Kasai, InnoALM and related models for pensions, Insurance companies and high net worth individuals. In: Zenios, S.A., Ziemba, W.T. (eds.) Handbook of Asset and Liability Management, vol. 2, pp. 861–962. North-Holland (2007)

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2010 Springer-Verlag Italia

About this paper

Cite this paper

Barro, D., Canestrelli, E. (2010). Tracking error with minimum guarantee constraints. In: Corazza, M., Pizzi, C. (eds) Mathematical and Statistical Methods for Actuarial Sciences and Finance. Springer, Milano. https://doi.org/10.1007/978-88-470-1481-7_2

Download citation

DOI: https://doi.org/10.1007/978-88-470-1481-7_2

Publisher Name: Springer, Milano

Print ISBN: 978-88-470-1480-0

Online ISBN: 978-88-470-1481-7

eBook Packages: Mathematics and StatisticsMathematics and Statistics (R0)