Abstract

This paper examines the net benefit accruing to a present-biased government contemplating the option of speeding up investment setting a lower tax rate on future profits or an investment subsidy as an incentive. The literature generally suggests the use of an investment subsidy rather than a reduced tax rate. However, this study shows that, depending on the degree of present-biasedness, it may be more advantageous for the government to set a lower tax rate. The government, in fact, when selecting the instrument to be used for speeding up investment, trades off the immediate and certain cost of a subsidy against the random tax revenues accruing from the investment. Hence, from the short-sighted perspective of current government, a lower tax rate may appear optimal as long as the consideration given to the earnings of future governments is small and/or the current government’s duration is short.

Similar content being viewed by others

Notes

This frame can also be easily adapted to the case where the investment cost, I, evolves randomly following a geometric Brownian motion (see e.g. Dixit and Pindyck 1994, pp. 207–211).

This frame can also be easily adapted to analysis of the case where profits are subsidised and an excise tax must be paid at the time of the investment.

For calculation of expected present value, see (Dixit and Pindyck 1994, pp. 315–316).

Convergence of the model requires the trend in profit not to exceed the discount rate, as otherwise investing would never be optimal for the firm.

The time index is dropped for notational convenience.

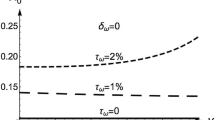

Note that \(\partial \gamma /\partial \rho >0,\ \partial \gamma /\partial \alpha <0\) and \(\partial \gamma /\partial \sigma ^{2}<0\).

In addition, all rival parties share the same time preferences.

Note that within frame (i) \(\lambda \) may represent the rate of intergenerational transition.

Note that by including \(\beta =1\) in the interval considered we are implicitly allowing also for the case of a non-present-biased government.

Note also that in our frame, differently from Sarkar (2012) where the government’s discount rate is assumed constant and higher than the firm’s rate, government \(G_{i}\) discounts future pay-offs at a rate higher than the one used by the firm but time-declining, i.e., \(\overline{\rho } _{i}(t,s)\ge \rho \).

The stochastic discount functional form in Eq. (5) is consistent with the continuous-time version of quasi-hyperbolic preferences introduced by Harris and Laibson (2013). The rate, \(\overline{\rho }_{i}(t,s)\), is the discount rate associated with the expected value of \(D_{i}(t,s)\) with the expectation taken with respect to the probability of a drop in the discount function occurring after time s, i.e. \(e^{-\lambda (s-t)}\).

As in Pennings (2000), government and firm are viewed as framed in a vertical relationship. The underlying two-stage game is solved by first determining the firm’s optimal investment timing strategy and second, moving backward, by letting the government sets the policy package consistent with its own targeted outcome.

This may very well be the case for countries where, after the global financial crisis and the European sovereign-debt crisis, governmental resources are scarce and/or strict rules imposing balanced budgets have been set (see Barbosa et al. 2016).

As can be easily proven, a policy package (\(\theta _{1},\theta _{2}\)) set by the government in order to maximize net revenues, on the basis of its own time preferences, i.e. \(R(\theta _{1},\theta _{2})\), is not consistent with the acceleration of firm investment.

See Pennings (2000) for further details.

References

Aguiar M, Amador M (2011) Growth in the shadow of expropriation. Q J Econ 126(2):651–697

Amador M (2003) A political economy model of sovereign debt repayment. Working Paper, Stanford University

Barbosa D, Carvalho VM, Pereira PJ (2016) Public stimulus for private investment: an extended real options model. Econ Model 52:742–748

Di Corato L (2012) Optimal conservation policy under imperfect intergenerational altruism. J For Econ 18(3):194–206

Dixit AK, Pindyck RS (1994) Investment under uncertainty. Princeton University Press, Princeton

Dosi C, Moretto M (1997) Pollution accumulation and firm incentives to accelerate technological change under uncertain private benefits. Environ Resour Econ 10(3):285–300

Harris C, Laibson D (2013) Instantaneous gratification. Q J Econ 128(1):205–248

Maoz YD (2011) Tax, stimuli of investment and firm value. Metroeconomica 62(1):171–174

Pennings E (2000) Taxes and stimuli of investment under uncertainty. Eur Econ Rev 44:383–391

Pennings E (2005) How to maximize domestic benefits from foreign investments: the effect of irreversibility and uncertainty. J Econ Dyn Control 29:873–889

Phelps ES, Pollak RA (1968) On second-best national saving and game equilibrium growth. Rev Econ Stud 35(2):185–199

Sarkar S (2012) Attracting private investment: tax reduction, investment subsidy, or both? Econ Model 29(5):1780–1785

Yu C-F, Chang T-C, Fan C-P (2007) FDI timing: entry cost subsidy versus tax rate reduction. Econ Model 24(2):262–271

Author information

Authors and Affiliations

Corresponding author

Additional information

L. Di Corato wishes to thank Yu-Fu Chen and the two anonymous reviewers for helpful comments. He is also grateful for comments and suggestions to participants at the workshop “Taxes, Subsidies, Regulation in Dynamic Models” (University of Brescia). The usual disclaimer applies.

Rights and permissions

About this article

Cite this article

Di Corato, L. Investment stimuli under government present-biased time preferences. J Econ 119, 101–111 (2016). https://doi.org/10.1007/s00712-016-0494-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00712-016-0494-4