1. Introduction

Floods are recurring natural phenomena [

1]. Floods can be caused by extreme rainfall events, sometimes in combination with snow melt inland or by storm surges in coastal area [

2]. Due to climate change, the frequency and intensity of extreme events is expected to increase globally, as reported in the fourth and fifth assessment reports of the Intergovernmental Panel on Climate Change (IPCC) [

3,

4]. In addition to extreme hydro-meteorological events, different anthropogenic activities, such as population growth, extensive urbanization, land use and poverty distribution, play an important role in producing catastrophic floods [

5]. As a consequence, globally, the number of large inland flood catastrophes between 1996 and 2005 was twice as large, per decade, than between 1950 and 1980, while the economic losses increased by a factor of five [

6].

The impacts of floods can be significantly reduced through a holistic approach to “flood risk management”. Flood risk management now is not only focused on technical measures, such as dyke systems, but also on reducing exposure and vulnerability [

7,

8]. The estimation of flood losses supplies crucial information to decision support and policy development in the fields of flood management [

9]. Depending on the degree of monetization (

i.e., characterized by market value) and the degree of physical contact with the hazard, flood losses can be classified into four categories: direct tangible, direct intangible, indirect tangible and indirect intangible losses [

9,

10]. Tangible losses can [

11] be estimated in monetary terms (all marketable goods and services), but intangible losses have no market value, e.g., loss of life, losses to ecosystems. Direct losses are those resulting from the physical contact of flood water with humans, property or any other objects (e.g., structural losses to buildings). Indirect losses are induced by the direct impacts, but occur, in space or time, outside the flooded area (e.g., costs occurring longer after the flood event or outside the flood-affected area) [

12]. The available methods for estimating flood losses are mainly focused on direct tangible losses of residential, industrial, agricultural and commercial sectors. Residential buildings are commonly strongly affected by floods [

13,

14].

Depending on the purposes, economic loss assessments can be categorized into

ex ante assessments and

ex post assessments. Using physical process-based models,

ex ante assessments aim to evaluate potential economic losses prior to possible events, while,

ex post assessments are carried out in the after-math of an event. Until recently, most economic analysis guidelines mainly addressed

ex ante assessments, while

ex post assessments are not as well developed [

14].

Flood losses are influenced by many variables, such as flood depth, flow velocity, flood duration, contamination, sediment concentration, lead time and information content of flood warning, building characteristics (elevation, structure,

etc.) and the quality of external response in a flood situation [

9]. However, most available loss models consider the water depth as the most important variable for economic loss assessments [

13,

15].

Stage-damage functions are a popular and simple method for loss assessment; however, studies have shown that they are associated with large uncertainty because the single variable only explains a part of the data variance [

15,

16,

17,

18]. Direct flood loss to buildings is influenced by more variables than inundation depth and building characteristics. For instance, flow velocity and flood duration are considered as influencing variables in the loss model HIS-SSM (High Water Information System-Damage and Casualties Module) [

19]. In a study in Australia, Smith [

20] found that warning time and type of building and content play a significant role in flood losses. The important roles of flood warning and preparedness in reducing flood losses are confirmed in studies in America [

21,

22]. Loss-determining variables can be classified into impact and resistance variables. Impact variables reflect the characteristics of the flood event at the affected object, while resistance variables reflect the characteristics of a flood-prone object. For example, flood experience, mitigation measures and early warning influence the resistance [

12,

15,

23,

24].

Quantifying the single and joint effects of these variables on flood losses is an important aspect for flood loss assessments and can be effectively undertaken by multi-variate loss analyses [

15,

18,

24]. A study based on loss data from the 2002, 2005 and 2006 floods in Germany revealed that the most important loss-influencing variables were water depth, floor space of building, flood return period, building value, contamination, inundation duration, precautionary measures and flow velocity [

18].

However, such a multi-variate analysis of flood loss data has so far not been undertaken for flooding in the Mekong delta. Vietnam, in the Mekong delta, is an example where floods occur on a recurring basis during the wet season (from July to November). The monsoon causes long-lasting floods and widespread inundations [

25]. Most of the settlements and infrastructures are located along river banks or flood protection dykes, so that floods lead to damage to exposed people, assets and infrastructures [

26]. Sea level rise and increased precipitation during the wet season are expected to be pronounced in the south of Vietnam [

27], resulting in increased frequency of flood hazards in the Mekong delta. In Can Tho city, the biggest city in the Mekong delta, sea level rise and precipitation increase in combination with urbanization is likely to significantly increase the pluvial flood risk [

26]. The extreme flood in 2011, for example, caused significant losses to buildings, businesses and infrastructure [

28]. Currently, there is no standard approach for flood loss assessments in the Mekong delta, including Can Tho city. Available loss assessment studies use stage-damage functions [

19,

29,

30].

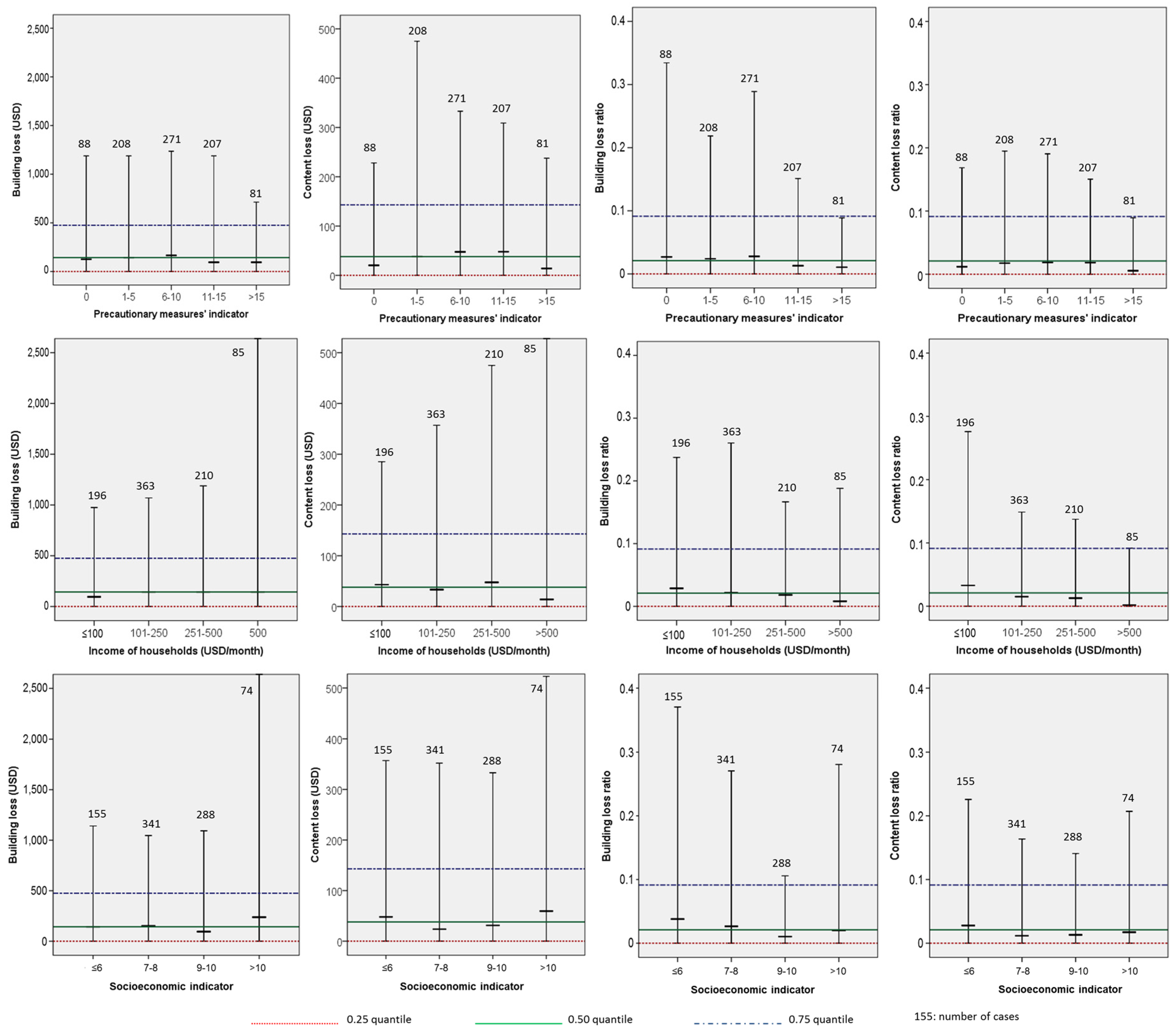

The objective of this study is to improve the quantitative knowledge about damaging processes and loss-determining variables for residential buildings in the Mekong delta, specifically in Can Tho city. The most important variables influencing flood losses are identified through multi-variate analysis considering 23 candidate predictors and the predictands for absolute flood loss of buildings and contents, as well as the loss ratio of buildings and contents. The loss data were compiled from interviews with 858 households and businesses damaged by the flood in 2011 in Can Tho city.

2. Study Area

In Can Tho city, riverine flood and tidal influences act together. River discharges are commonly high from September to November, whereas the flood tide is strong from October to January. The flood in 2011 was a severe one in Can Tho city causing great damage to agriculture, infrastructure, buildings and business. During the flood event in 2011, some areas close to the river were inundated continuously for nearly a month; other parts of Can Tho city were recurrently inundated for several months. Overall, about 27.8 thousand houses were inundated, and an economic loss of 11.3 million U.S. dollars occurred to buildings, infrastructure, agriculture and aquaculture [

28].

Data collection was undertaken by interviews with 480 flood-prone households and 378 small businesses (which are located in a type of shop-house, including a living part and a business part) in four urban districts of Can Tho city, namely, NinhKieu, BinhThuy, Cai Rang and O Mon [

28]. To identify the sample area, qualitative expert interviews were conducted with flood-damage experts and housing experts. A quantitative survey method was used for the household interviews. The questionnaire (online

Supplementary Material) covered the following topics: characteristics of the 2011 flood event, flood preparedness, warning and emergency measures, losses to households’ content and building structure, risk perception, as well as socioeconomic characteristics of the respondents. Each topic contained several questions, and altogether, there were 70 questions for households and 88 questions for small business. For the interviews related to small business, the questionnaire consisted of two parts: questions related to the living part focusing on the building and contents and questions related to the business part focusing on goods, equipment and sale. In this paper, only answers to questions related to the living part were taken into account. Therefore, all data collected via household and business interviews were combined into one database containing information on flood losses to buildings and contents and potentially influencing variables. The interviews were undertaken in January to February 2012, right after the flood event. In order to improve the quality of the collected data, cross-checks between answers to different related questions were performed, for instance comparing estimates of losses with estimated building and content values. More details about the survey and collected data were published by Chinh

et al. [

28].

5. Conclusions

To improve the knowledge about damaging processes and to quantify the effect of the important loss-influencing variables, multi-variate statistical analysis is carried out for flood loss data from the 2011 flood in Can Tho city, the biggest city in the Mekong delta. For data collection, 858 flood-affected households and small businesses were interviewed.

Our results reveal that under the specific flooding situation in the Mekong delta with relatively well-adapted households, long inundation durations and shallow water depths, inundation duration is more important than water depth for the amount of resulting loss. Additionally, building variables, such as building or content value, floor space of the building or building quality, also significantly influence the loss ratios. According to our results, precautionary measures play a key role in flood loss mitigation, in contrast to the emergency measures. The household characteristics, such as socioeconomic status or income, strongly influence building and content losses, probably also due to their strong correlation with the building quality and value.

The knowledge gained on damaging processes is helpful for recovery issues and for adapting the flood risk management strategy on the basis of the experiences with the flood in 2011. However, particularly, the results have important implications for loss estimation and flood risk assessments. Commonly, depth damage functions are used for flood risk assessment all over the world, and often, published functions are transferred in time and space without checking their suitability for the specific application and region. Our results suggest that for areas like Can Tho city in the Mekong delta, depth damage functions are not suitable. Instead, multi-variable loss models may be a better option, since they are better able to represent complex damaging processes.

and

and

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}